The Number Everyone Compares Is the Wrong Number

Open any real estate platform that covers multiple countries. Sort by rental yield. I am sure you will get a nice and tidy ranking: this market at 8%, that one at 6%, another at 5%.

Clean, comparable, easy to act on. It also makes you feel as if you are doing some serious research.

Except it is not comparable at all.

That number is gross yield, in other words, annual rent divided by property price. It tells you what the property earns before anyone takes their cut. And in domestic investing, where tax rates and borrowing costs are roughly the same across your options, it is a perfectly fine "rule of thumb" metric to look at.

But the moment you are comparing across borders, gross yield stops being a useful signal and starts being a trap that can lead you down the wrong path when selecting your best options.

What gross yield actually ignores

There are two things that vary enormously between countries and that sit directly between your gross rent and your actual cash flow:

The tax you pay on rental income

The cost of the money you used to buy the property (assuming you are using some degree of financing)

Rental income tax rates are not the same across different countries. You might pay 15% on rental income in one and 42% in another.

This is the reality you would face only after already investing your time and money, which is well... too late.

Then there is the cost of borrowing. If you financed part of the purchase (and most people do, the assumption we use on the platform is 20%), the local interest rate matters for you, as it is a fixed cost you would have to pay regardless of your rental yield.

And just like the tax rates, local interest rates are not the same everywhere. A market with 4% rates and a market with 8% rates will produce radically different outcomes from the same gross yield.

Put those together and the gross number becomes almost decorative. It is the yield you would earn in a world where governments do not tax rental income and banks lend for free. That world does not exist. Or if it does, we would surely want to hear more about it.

Same number, different reality

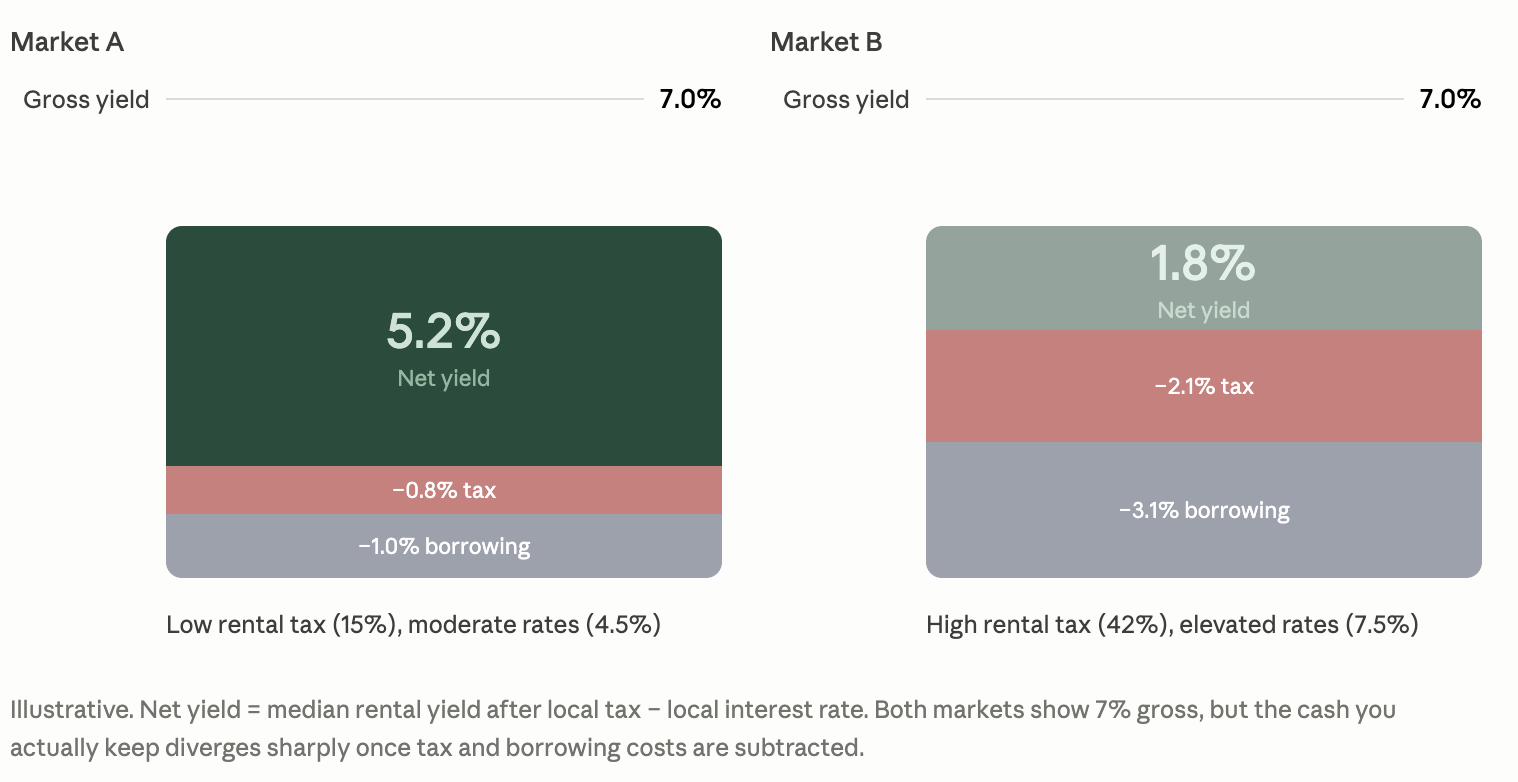

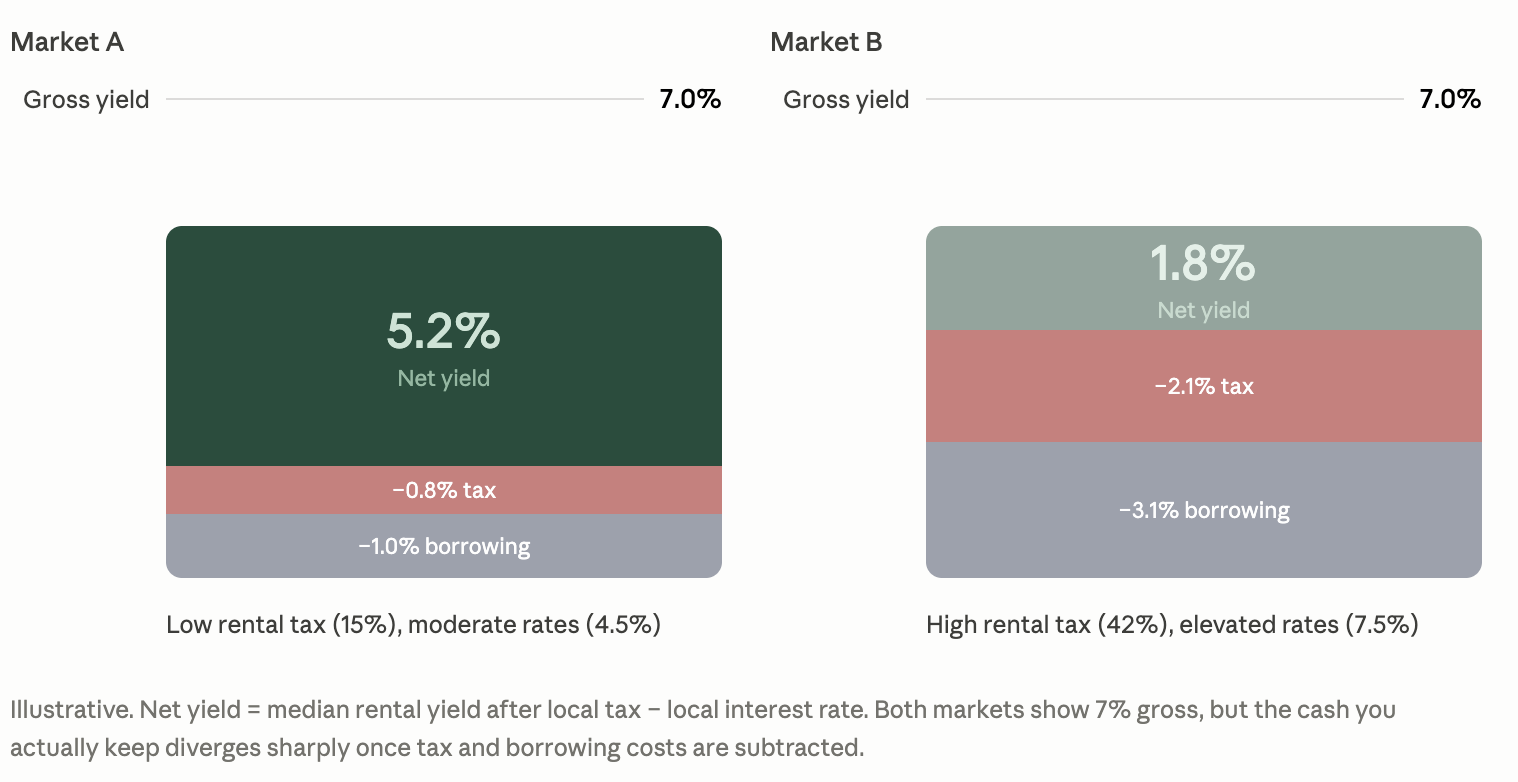

Here is what this actually looks like with concrete figures.

Both markets report a 7% gross yield. An investor who sorts by gross yield would rank them equally. But Market A has low rental tax and moderate interest rates, so you keep 5.2% after costs. Market B has steep rental tax and expensive borrowing, you keep 1.8%.

That is a 3.4 percentage point gap hidden inside a number that looked identical. If we assume both properties had a cost of EUR 500,000, that is EUR 17,000 difference in what you actually put into your pocket each year. It is the kind of gap that turns a good investment into a mediocre one, or vice versa, without the gross yield ever hinting that something was wrong.

Why everyone still uses gross yield

Honestly? Because it is easy to calculate and easy to find. Rent divided by price. Every listing has both numbers. You can compute it in your head over coffee.

Net yield is harder. You need the local tax rate on rental income for non-residents (which is often different from the rate for locals). You need to know the prevailing mortgage rate for foreign buyers in that market (also often different). You need to make an assumption about leverage. And you need to do this consistently across every market you are comparing, or the comparison is just as broken as the gross number.

Most platforms do not really care. They either show gross yield and let you figure out the rest, or they skip yield entirely and show you property prices, which tells you even less about what you will actually earn.

What we built instead

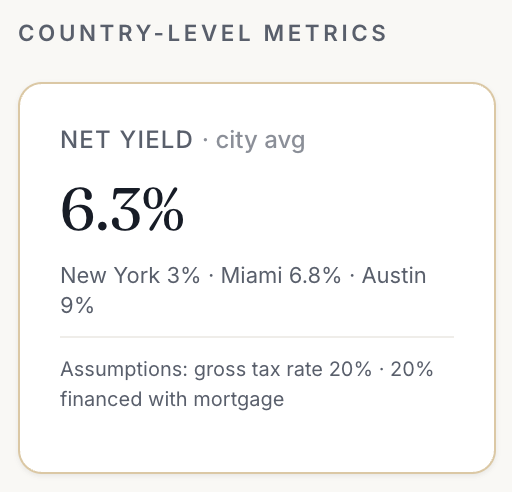

This is one of the metrics we spent the most time on when designing the platform. Our net yield calculation works like this: take the median rental yield in the market, subtract the local tax rate on rental income, then subtract the local interest rate (weighted for a standard financing assumption of 20% leverage at a 20% tax rate). What is left is the yield the market actually pays you in real terms.

It is a single number, but it is comparable across different countries and cities, allowing you to better set your expectations for what kind of ROI you can expect.

Of course, we did not invent this concept. Any serious institutional investor adjusts for tax and financing before comparing markets. The difference is they have analysts doing it in spreadsheets, and we are doing it once, consistently, so you do not have to.

INSIGHT: A gross yield is a property fact. A net yield is an investor fact. One describes the building. The other describes what happens to the money after the building, the government, and the bank have all had their say.

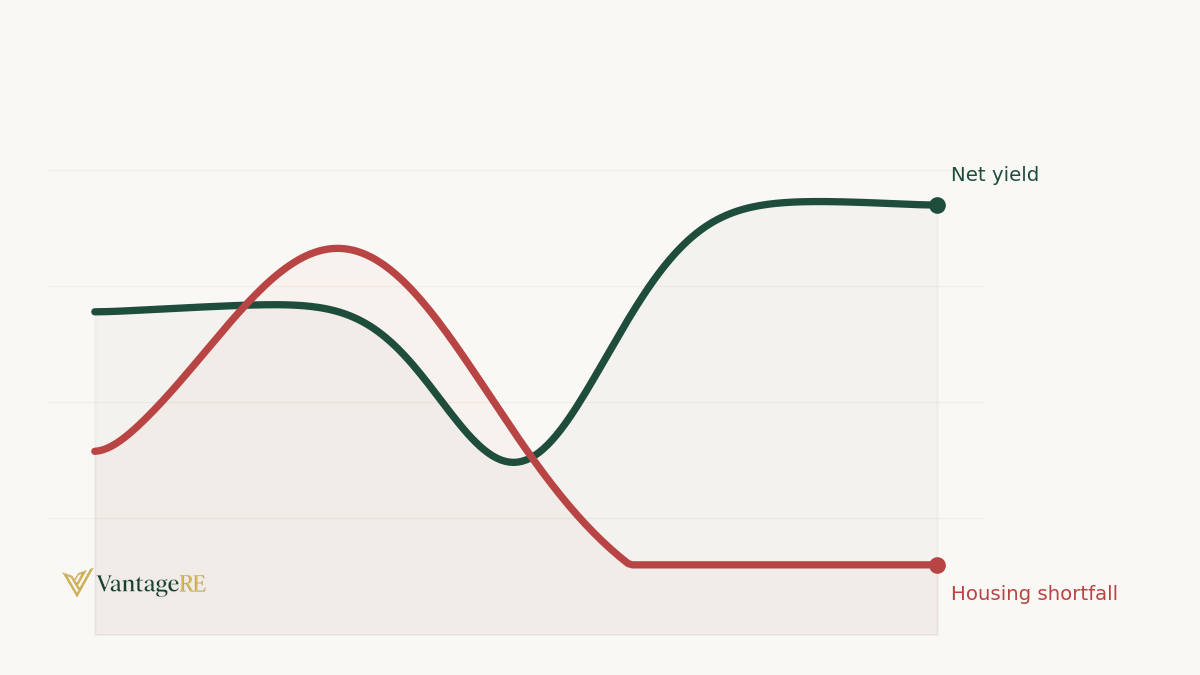

Where it matters most

The gap between gross and net is not uniform or even as intuitive as you might think.

High-tax countries with elevated interest rates (parts of Western Europe, for example) often report perfectly reasonable gross yields that collapse once you layer in the deductions. Meanwhile, markets with low or zero income tax and moderate rates (parts of the Gulf, certain Southeast Asian markets) tend to preserve most of their gross yield through to the bottom line.

This means that gross yield rankings do not just get the absolute value of what you will earn wrong. They can get the priority/profitability order wrong. A market that looks average on gross yield might rank first on net yield, because it keeps more of what it earns. And a market that tops the gross ranking might fall to the bottom once you account for what the government and the bank take.

If you are comparing domestically, two neighbourhoods in the same city, gross yield is fine. Same tax rate, same borrowing costs, the deductions cancel out.

But the moment you are looking across a border, gross yield is actively misleading, because the things it ignores are exactly the things that vary.

The short version

Do not compare markets by what they earn before costs. Compare them by what they keep after costs.

The difference between gross and net yield is the difference between looking at a menu and looking at a bill.

One of them has the tax on it.

The VantageRE research team writes on cross-border property, tax, and residency. Independent, no sponsored coverage, no sales scripts.

Join the VantageRE private beta — country pages, comparison tools, and live datasets.